How to Create a Nonprofit Operating Budget

Each nonprofit organization has its mission, set of programs, corresponding financial framework, and, importantly, an operating budget.

Helping Hands Monkey Helpers, for example, is a charity dedicated to pairing trained service monkeys with individuals suffering from mobility impairments. The organization manages the costs associated with overseeing each monkey’s training, service, and lifetime needs.

Additionally, the Tall Clubs International Foundation financially supports exceptionally tall members of society. This organization raises, manages, and disperses scholarship funds for tall individuals entering their first year of higher education.

Clearly, the needs of society are incredibly diverse. . . and often quite strange. So, whether you’re training service monkeys or supporting the exceptionally tall, you need an operating budget that reflects your organization’s unique needs.

This article will discuss how to craft an operating budget tailored to your needs and requirements. Here’s exactly what we’ll cover.

Track Your Revenues and Expenses with this Operating Budget Template

Use this template to create an operating budget and monitor your nonprofit’s financial performance during this fiscal year.

What is a Nonprofit Operating Budget?

Put simply; an operating budget outlines an organization’s revenue and expenses for a fiscal year.

An operating budget is essential for your organization because it helps organize short-term goals. Additionally, budgeting provides a transparency mechanism, as it can communicate the management of resources to your stakeholders.

What’s more, when creating your budget, you will find gaps in your operations where you could potentially save money or invest more. During this process, you will also benefit your organization by deciding what operations best advance your organization’s mission.

Operational revenue and expenses are the critical components of an accurate and helpful operating budget.

When determining revenue, nonprofit professionals should forecast the resources their organization is likely to acquire. In the for-profit world, revenue is typically classified as resources earned from the sale of goods and services.

Many nonprofits receive a lot of their revenue from activities that can be considered the sale of goods and services. These are activities like contracting out their services, selling memberships, providing fees for services, or selling merchandise and other goods.

However, nonprofit revenue often comes from other forms of support such as donations, grants, and different types of contributions. So, nonprofit revenue can be divided into traditional revenue (sales and services) and other forms of support (donations and grants). For more information on generating other forms of support, check out Keela’s comprehensive fundraising guide.

When determining operating expenses, nonprofit professionals should forecast their organization’s resources needed to carry out its activities during a fiscal year.

Here’s a list of operational expense categories that are important to consider:

- Staff salaries and benefits

- Rent and utilities

- Equipment and supplies

- Communications

- Insurance

- Meetings

- Travel

- Marketing and advertising

- Training and development

- Contracted-in services

- Legal

- Accounting

- Fund development

- Miscellaneous

At the end of a fiscal year, a nonprofit will likely end up in a profit or loss position. A profit, or surplus, is the excess of revenues over expenses. Conversely, a loss, or deficit, is an excess of expenses over revenues.

Nonprofits aim to generate a modest profit to preserve their financial sustainability. Having a carefully thought-out budget is one great way to get your organization going in that direction.

How to Create an Operating Budget for Your Nonprofit

Creating an operating budget begins where all nonprofit decision-making should begin: the organization’s mission.

Every nonprofit has a mission, usually one that is quite broad. Let’s take the organization Contributing to the Lives of Inner City Kids (CLICK) as an example. CLICK works to raise funds for programs that support inner-city kids in Vancouver. Here’s its mission statement:

CLICK’s mission is to engage the community by raising funds for programs that support inner-city kids so they can succeed.

Based on this statement, CLICK’s board of directors will have to determine specific objectives to achieve this mission. These objectives will lead to the creation of relevant programs or services which will have corresponding costs and revenue opportunities. These considerations, in combination with revenue forecasts, will make up the operating budget.

Predict Your Fundraising Revenue with this FREE tool

Use our fundraising forecasting tool to accurately forecast major gifts, grants, recurring donations, and more!

What is the difference between an Operating Budget vs. a Capital Budget?

Some confusion occurs when differentiating short-term and long-term objectives. This confusion brings us to a point where we need to differentiate between capital budgeting and operating budgeting.

Capital budgeting is the process of making long-term capital asset investments and financing decisions. Capital assets are long-lasting assets that advance the organizational mission and assets, i.e., land, facilities, and costly equipment. These are sometimes considered fixed costs.

Capital assets have to last more than a certain period and cost more than a threshold amount determined by an organization. Each organization will have a different definition of a capital asset. A $5,000 copier machine could be a capital investment for a small organization while also below the threshold of a large organization.

Capital and operating budgets both support the organization’s mission by planning and managing resources. However, procedural differences exist between them. For example, capital investments typically take more than one fiscal year to pay off, which must be conveyed when budgeting.

Be aware that the capital and operating budget have a close relationship. Investing in a capital asset often results in indirect costs for operation and maintenance. Nonprofits should be prepared for the impacts of capital acquisitions, even if the assets are donated.

How to calculate your operating budget

The easiest way to identify your operations budget is by looking at past behavior. Many nonprofit professionals do this by calculating their spending baseline: how much it would cost to maintain their current operations without changes to the previous year’s budget.

The spending baseline is typically calculated during the auditing phase of the budget cycle, which we will discuss below.

Another way to determine your operating budget is by splitting up the work. Consult your board, staff, and volunteers to understand what resources they require to effectively fulfill your organization’s mission.

Using both of these strategies will help your organization to stay closely aligned with its mission.

If you’re also wondering how to calculate your cash flows, download Keela’s cash flow forecasting tool! Use this simple resource to help balance your books and reduce your financial worry.

Create Your Nonprofit’s Operating Budget with this FREE Template

Use this template to create an operating budget and monitor your nonprofit’s financial performance during this fiscal year.

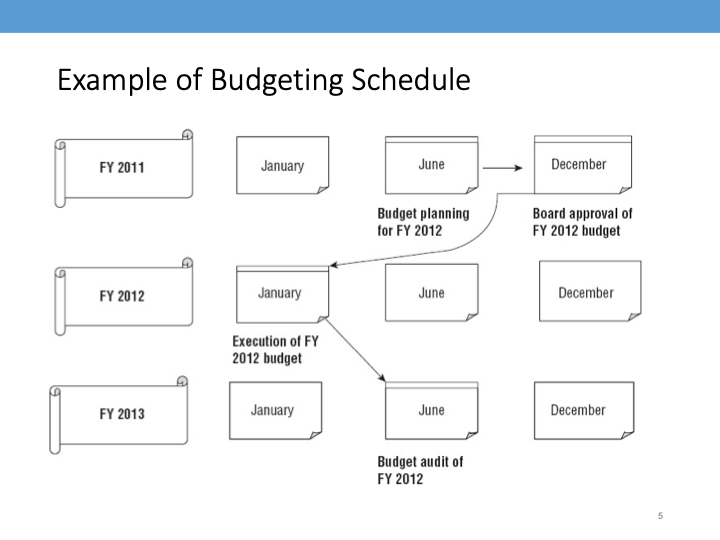

The Nonprofit Budget Cycle

An operating budget is determined throughout the budget cycle.

A fiscal year’s budget can have a total lifespan of up to 2 years. The planning of an operating budget begins up to half a year before the budget will be implemented. At this stage, the budget is referred to as the proposed budget.

Once the board of directors accepts the proposed budget, it is referred to as the adopted budget. Throughout the fiscal year, the adopted budget is referred to as the operating budget.

The budget’s name changes to “operating budget” because the organization may alter the adopted budget throughout the fiscal year. The organization will then operate with a budget that is no longer the exact adopted budget.

Last, up to half a year after the operating budget’s fiscal year, an audit will occur. This audit will determine if the previous year’s resources were managed appropriately and inform the following year’s budget.

This cycle will continue for the course of an organization’s lifetime.

Take a look at a visualization of the budget cycle below:

Nonprofit Operating Budget: Frequently Asked Questions

1. What is a good operating margin for a nonprofit?

There is no such thing as a “good” operating margin for a nonprofit. Every organization is different and therefore requires an extra degree of operating efficiency.

Operating margins are much more critical for companies as they demonstrate whether sales are efficiently being turned into profits. This for-profit margin is typically calculated by dividing a company’s operating income by its net sales. Higher ratios are generally better.

However, this ratio is not as crucial for nonprofits as they aren’t necessarily focused on efficiency. After all, nonprofits are created to maximize impact, not to maximize profit for shareholders.

Taking the above into consideration, let’s explore a brief example of a nonprofit operating margin calculation. The operating margin will demonstrate the efficiency of the organization’s day-to-day operations. This is calculated by dividing operating profits by operating revenue.

FYI, to determine your operating profits (or losses), simply total your revenue less your expenses.

The result of the operating margin calculation will be a decimal representing the percentage of profits yielded from operations. Simply multiply the decimal by 100 to get a clean percentage that represents your operating margin.

For example, let’s say a nonprofit has $1,000 of revenue and $40 of operating profits,

The nonprofit would divide 1,000 by 40 to get a result of 0.04. After multiplying this result by 100 and tacking on a percent symbol, the nonprofit understands its operating margin is 4%.

Want to boost your operating margin? Download the fundraising KPIs toolkit. Keela and Imagine Canada’s Grant Connect have teamed up to provide the essential fundraising metrics to ensure long-term financial success.

2. What percentage of a nonprofit budget should be salaries?

Like the above answer, every organization will have a different percentage of their budget for salaries.

Don’t let your organization determine its staff’s salaries based on a percentage that someone else made up!

A better way to understand how much you should pay staff is by analyzing the industry standards for certain positions. Check out Keela’s guide to nonprofit salaries to understand more about what to pay your team.

See How Nonprofits Use Keela to Raise 4x More!

Get a glimpse of how Keela’s donor management system can help you develop better relationships, retain donors and raise more for your cause.

As I hope you now see, a lot goes into determining a nonprofit operating budget. While drafting yours, remain mission-focused, involve your stakeholders, and use Keela’s operating budget template.